Of the approximately 60,000 high school students that graduated from a Maryland public school in 2013, over 33,000 either graduated from college with an Associate's or Bachelor's degree or discontinued their education without graduating five years after college[1].

The student loan [2] amounts for 5,000 were evaluated in the context of their wages. These students were selected as they were fully-engaged in the workforce five years after high school graduation[3].

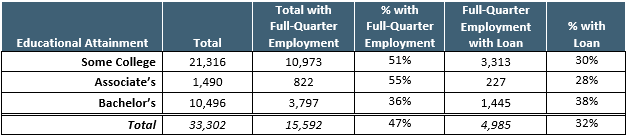

The percentage of students in each educational attainment group that had student loans varied from a low of 28% (Associate’s) to a high of 38% (Bachelor’s). See Table A.

32% of students with an Associate's degree, Bachelor's degree or Some College with full-quarter wages [3] have a student loan.

Table A. High School Graduates, State of Maryland, 2013, Full-Quarter Employment and Student Loans, Five Years after High School Graduation

The slightly lower rate for student loans for Associate’s students (Table A) is not surprising as these programs are typically two years in length and offered at community colleges. The short term of enrollment and the low tuition rates most likely decreased reliance on student loans to finance the education costs.

Conversely, those in the Some College or Bachelor’s (Table A) groups had longer periods of enrollment and/or paid higher tuition rates which most likely increased reliance on student loans to cover education costs. These results, particularly for Some College and Bachelor’s, should be viewed with caution. Approximately 27% of Maryland high school graduates enroll in college out-of-state and student loan data are not available for these students, therefore the actual number of students with loans is likely higher than what is reported here.

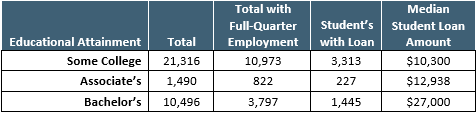

Table B. High School Graduates, State of Maryland, 2013,Full-Quarter Employment and Student Loans, Five Years after High School Graduation

The median loan amount for each educational attainment group varied widely [4]. See Table B. The median was lowest for Some College, around $10,000, and highest for Bachelor’s, around $27,000. The median for the Associate’s group fell in between, around $12,000. These medians align to the loan limits that the federal government establishes for each year of college enrollment. For example, the current federal student loan limit for first year undergraduates is $5,500 and for second year is $6,500, therefore a student with two years of undergraduate study, like those in an Associate’s degree program, may have a maximum federal loan amount of $12,000.